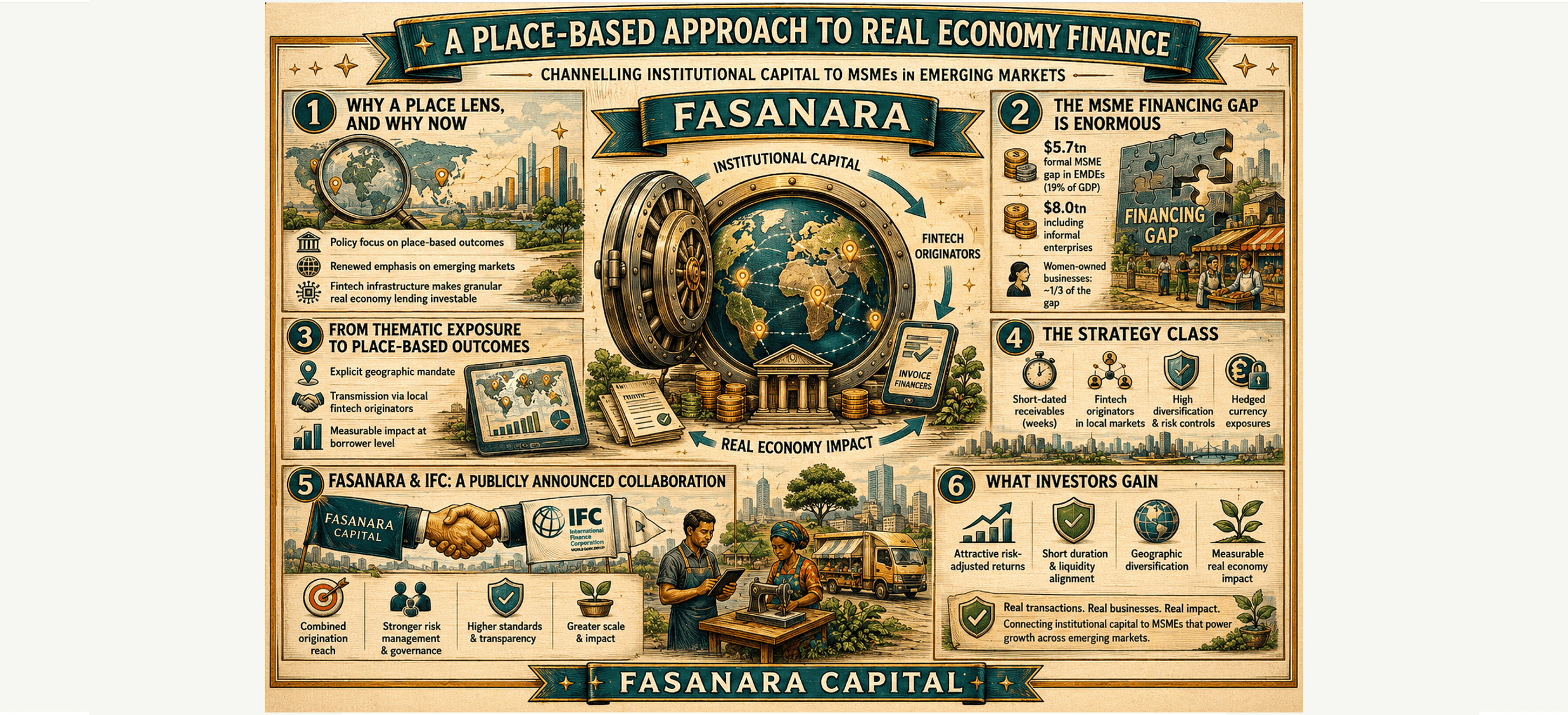

blog

A Real Economy Approach to Finance:

Channelling Institutional Capital to MSMEs in Emerging Markets

Why fintech-enabled receivables finance in emerging markets matters for thematic allocators.

Oliver Wade, Senior Investment Writer

27 May 2026

Why local growth matters now

Capital allocators are increasingly being asked to think geographically as well as thematically. Pension schemes, insurers and sovereign investors face mounting expectations to demonstrate where, not only what, their capital finances. This shift reflects three converging realities: a sustained focus on local growth and regional resilience in domestic markets such as the UK; a renewed emphasis on emerging market investment as a route to growth and diversification; and the maturation of fintech enabled credit infrastructure that, for the first time, makes very granular, geographically targeted real economy lending observable and investable at institutional scale.

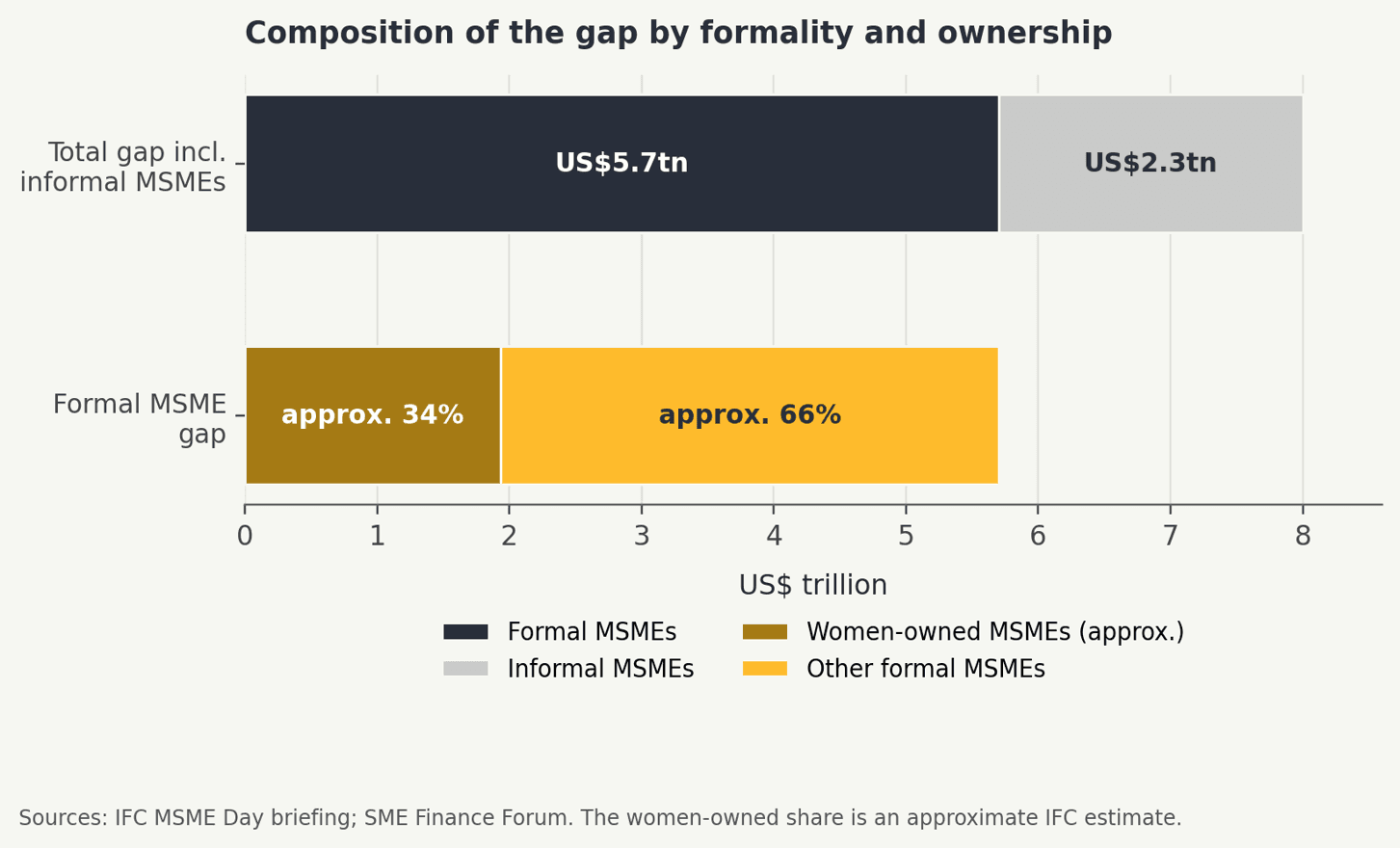

Within that broader context, one structural shortfall stands out. Micro, small and medium-sized enterprises (MSMEs) account for over 90% of firms, around 70% of employment and approximately 50% of GDP worldwide, yet in emerging markets and developing economies (EMDEs) they continue to operate against a multi-trillion-dollar financing gap. The most recent IFC and SME Finance Forum analysis, published at the end of 2025, estimates the formal MSME financing gap at approximately $5.7 trillion, equivalent to around 19% of EMDE GDP. Including informal enterprises, the gap rises to approximately $8.0 trillion. Women-owned businesses are disproportionately affected, accounting for around one third of the unmet financing need.

For investors, this is more than a development statistic. It defines the addressable market for a class of short duration, real economy credit that has historically been difficult to access from a developed market portfolio. The combination of a structural funding shortage, a digitising fintech origination layer and a growing demand for measurable local economic outcomes provides the conditions in which a dedicated emerging markets MSME strategies could potentially be both.

From thematic exposure to real economy outcomes

Most institutional capital that reaches emerging markets does so through public market beta, listed equity, hard currency sovereign bonds or large corporate credit. These channels are deep and liquid, but they tend to concentrate capital in the largest issuers and the most internationalised parts of the economy. They are not always the most effective conduit for capital intended to reach productive activity in local economies.

A real economy allocation framework, in our view, requires three things in combination. First, an explicit geographic mandate, with portfolio guidelines that define the eligible universe and the diversification framework. Second, a transmission mechanism that allows institutional capital to reach the intended end users, in this case MSMEs, through originators that are operationally embedded in local markets. Third, a measurement framework that links the capital deployed to the outcomes observed at borrower level, with reporting that is detailed enough to be auditable by an external party.

Fintech enabled receivables financing maps cleanly onto each of those requirements. Originators sit within national payment and invoicing ecosystems and serve borrowers whose business activity is, by definition, local. The underlying assets are short dated, contractual and self-liquidating, which limits asset-liability mismatch in a portfolio aiming for quarterly liquidity. And because each invoice and each borrower can be tagged at the asset level, the resulting development indicators reflect actual transactions, not assumptions.

The strategy class, and a publicly announced collaboration

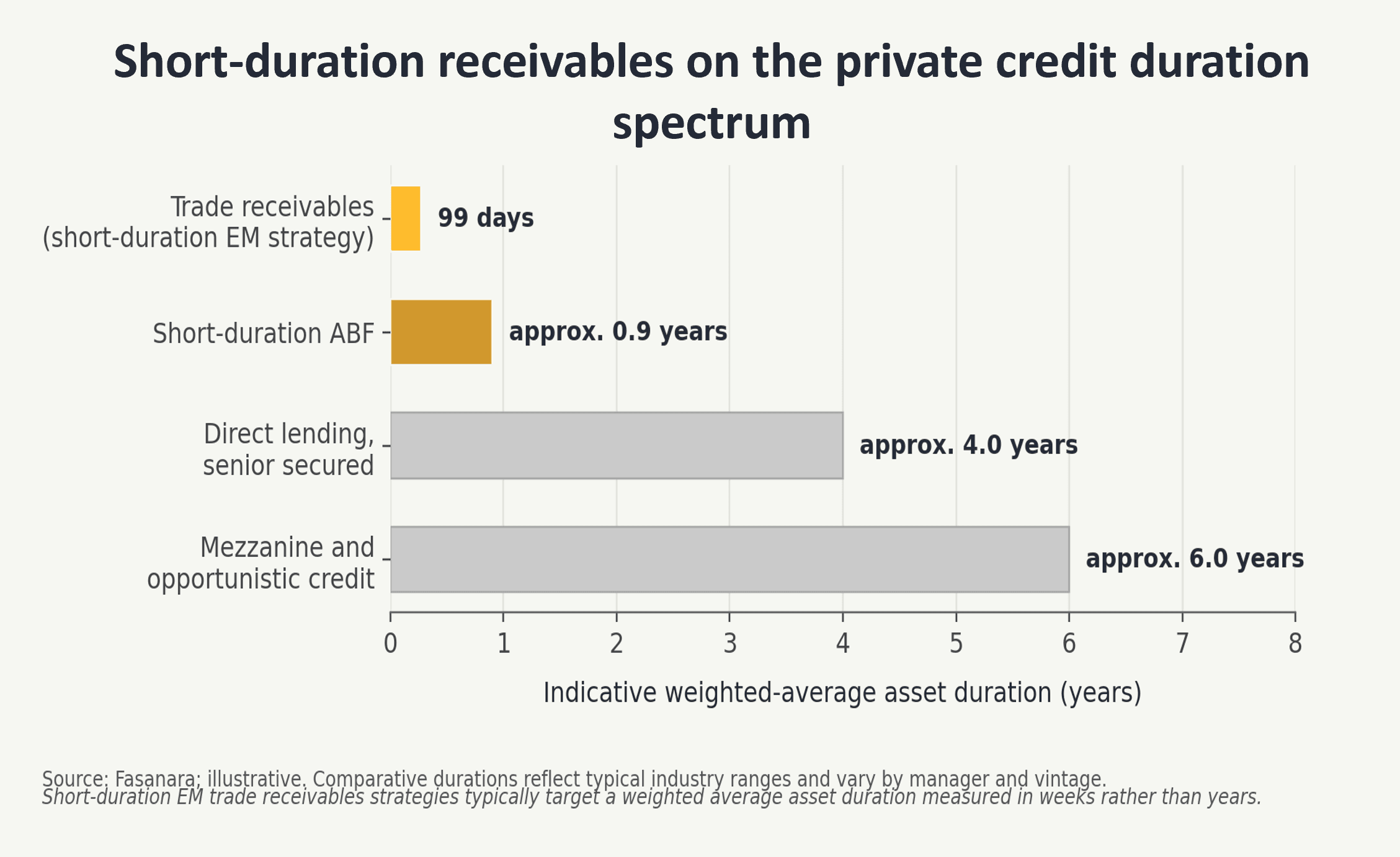

Fintech enabled receivables financing in emerging markets can be described, as a strategy class, by a relatively consistent set of design features. Capital is deployed into short-dated trade receivables and digital invoices generated by MSMEs, purchased through technology-enabled originating platforms that are operationally embedded in local economies. Average asset duration is typically measured in weeks rather than years. Diversification is engineered through country, originator, debtor and industry limits, with hedging where currency exposures are not naturally aligned to the investor base. The result is a portfolio of many small, contractual exposures rather than a concentrated book of larger loans.

In March 2026, Fasanara Capital and the International Finance Corporation (IFC), a member of the World Bank Group, established a cooperation framework to explore mechanisms for expanding access to finance for small and medium-sized enterprises (SMEs) across emerging markets, particularly those that are women-owned and women-led. The stated objective is to channel institutional capital through fintech originators to support real-economy lending.

Discipline as a design feature

Granularity, diversification and disciplined originator selection are central to how strategies of this kind behave. They take on additional importance in an emerging markets context, where individual country, sector or originator concentration can translate into outsized tail risk. Institutional implementations typically codify this through explicit, ex-ante portfolio guidelines rather than discretionary risk management.

Several features tend to be common across well-constructed examples. Country exposure is capped, with tighter limits applied to lower-rated jurisdictions. Single-debtor and single-seller limits keep individual borrower exposures in the low single digits as a proportion of net asset value. Originator exposure is similarly capped, and originators are subject to minimum quality thresholds, with onboarding and monitoring informed by asset-level data feeds. Currency exposures are hedged into the base currency of the investor. Cash balances are bounded, with deviations permitted only under defined abnormal market conditions. Where strategies build through a ramp-up period, looser limits during initial portfolio construction step down to tighter steady-state ceilings, an architecture that preserves flexibility without weakening the long-term diversification profile.

The cumulative effect is intended to be a portfolio of many thousands of small, contractual exposures, sourced across multiple jurisdictions and originators, with no single name dominating the loss distribution. Granularity does not eliminate credit risk, but it changes its shape, and it is the structural feature that most distinguishes this strategy class from a concentrated emerging markets corporate book.

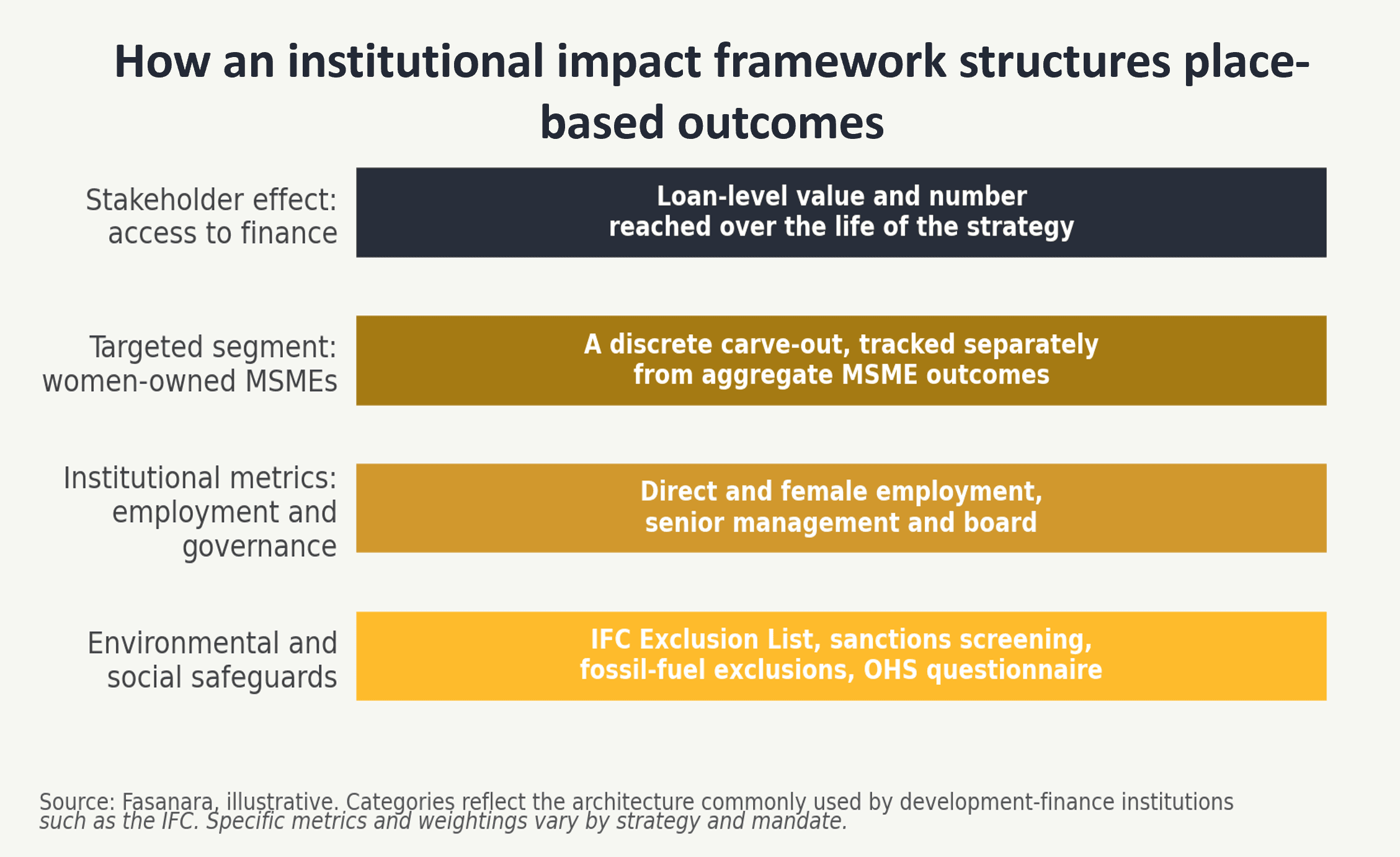

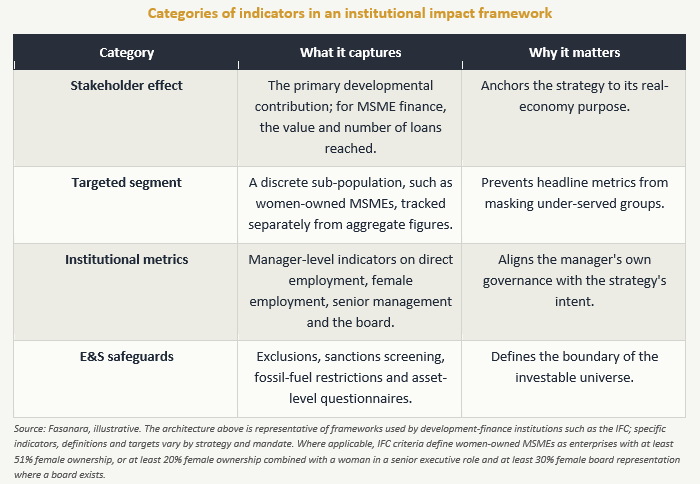

Measuring real economy outcomes

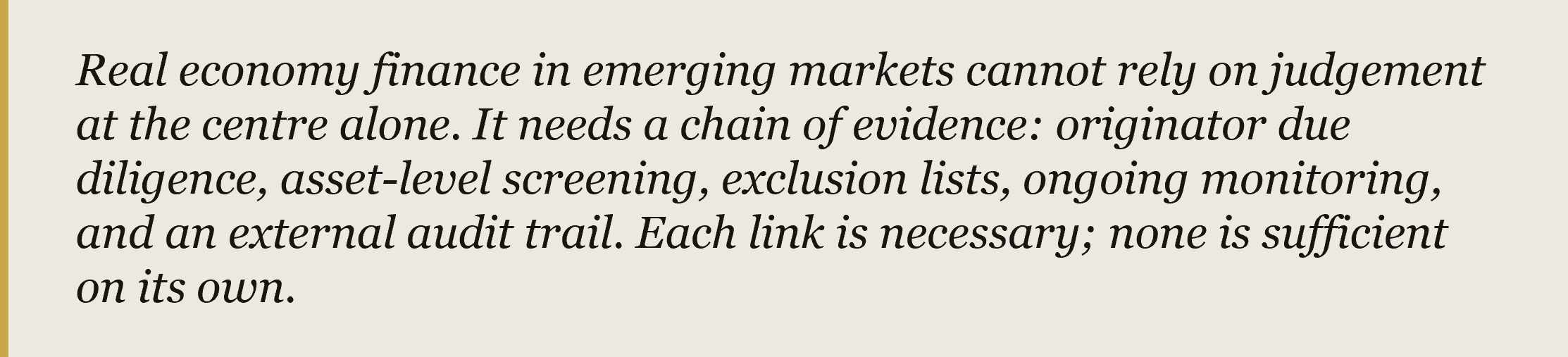

A distinguishing feature of partnerships with development-finance institutions is the requirement for measurable outcomes, agreed ex-ante and tracked over the life of the investment. Frameworks of this kind, used by the IFC and similar institutions, typically share a common architecture: a stakeholder effect that captures the primary developmental contribution, one or more targeted segment indicators that carve out specific sub-populations, institutional metrics covering employment and governance at the manager level, and a set of environmental and social safeguards that govern the eligible universe.

Two features tend to distinguish institutional frameworks from more conventional reporting. Indicators are explicit ex-ante targets, not retrospective narratives, with sub-population outcomes carved out separately rather than embedded in aggregates. And reporting flows from the asset level upward, so that each underlying invoice or loan can be tagged to a borrower and aggregated against the indicator set, supporting clear accountability and external audit.

Governance and safeguards

A locally anchored strategy with developmental objectives lives or dies on its governance. Three layers tend to be present in well-constructed examples. At the vehicle level, independent operational infrastructure, an external administrator, a depositary and an external auditor support the controls expected of a regulated alternative investment fund. At the strategy level, advisory or oversight bodies provide a forum for strategic review, conflicts management and valuation discussion, with explicit information rights for institutional investors. At the manager level, alignment is reinforced through manager co-investment and seed capital from related vehicles.

Environmental and social safeguards are typically integrated into the eligible universe rather than overlaid afterwards. Investments are screened against the relevant sanctions lists and exclusion frameworks. Where development-finance partners are involved, fossil fuel related activities, including coal, peat, oil and gas exploration and production, fuel oil-fired power generation and any infrastructure exclusively dedicated to the transport or storage of coal, peat or oil, are typically excluded. Higher environmental and social risk activities are subject to additional screening, and questionnaires capturing occupational health and safety, labour and working conditions at the MSME level can be incorporated into onboarding. The intent is to bring institutional discipline to a segment of the market where standardised safeguards have historically been uneven.

Portfolio relevance for institutional allocators

Strategies of this kind do not substitute for core direct lending or for liquid emerging market debt. They may, however, complement an existing private credit allocation in a number of respects. The first is duration: with weighted average maturities measured in weeks, exposure is structurally short relative to most private credit, limiting sensitivity to rate moves and creating a continuous reinvestment cycle. The second is granularity: a portfolio designed to reach tens of thousands of small loans is, by construction, less exposed to single-name idiosyncratic events than a concentrated book of larger loans.

A third dimension is diversification within emerging markets. Sourcing across multiple countries, sectors, originators and currency zones, with hedging where required, may behave differently from concentrated emerging market hard currency credit, although correlations can rise in periods of broad market stress. A fourth is real economy reporting: allocators with explicit geographic, gender or development objectives can map portfolio data directly to those objectives, supported by the indicator architecture described previously.

None of these features eliminates the inherent risks of investing in emerging market private credit. They are intended to make those risks visible, bounded and reportable, so that allocators can assess the strategy class on its own terms rather than as a generic emerging markets exposure.

Conclusion

A place lens is not a marketing label. It is a discipline that asks the capital allocator to specify where finance is intended to land, what evidence will demonstrate that it has done so, and how the strategy will respond when conditions change. Applied to emerging market MSMEs, that discipline runs into a structural reality: a US$5.7 trillion financing gap in formal MSMEs, around one third of which is borne by women-owned businesses, and a fintech origination layer that is now capable of intermediating institutional capital at scale.

Disclaimer

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell, or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investors or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with their financial professionals. The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance does not predict or guarantee future results. Investing involves risk; principal loss is possible. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. Fasanara Capital Ltd, is authorised and regulated by the Financial Conduct Authority (“FCA”).

Important information on risk

Investing involves risk. The value of any investment and the income from such can go down as well as up, and you may not get back the full amount invested. Changes in the rate of exchange may also cause the value of overseas investments to go up or down. This information represents the views of Fasanara Capital Ltd and its investment specialists. It is not intended to be a forecast of future events and/or guarantee of any future result. Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. There is no assurance that an investment will provide positive performance over any period of time. This information does not constitute investment research as defined under MiFID.